If your business operates across borders, even occasionally, you already know how complicated global money management can be. Exchange rate fluctuations, additional fees, delayed transfers, and juggling multiple bank accounts can quietly eat into your margins and your time.

A multi-currency account can help solve that problem.

In this guide, we’ll walk you through what multi-currency accounts are, how they work, their key benefits and challenges, and how to choose the right provider for your business. We’ll also explore how modern platforms like OFX are redefining global financial management by bringing domestic and international payments into one platform. One solution for full payment control.

What is a multi-currency account?

A multi-currency account allows you to hold, send, and receive funds in multiple currencies from a single platform.

Instead of opening separate foreign bank accounts in different countries, you can manage several currencies in one consolidated dashboard.

This eliminates unnecessary conversions and gives you more control over your foreign exchange (FX) strategy. Plus, having an integrated multi-currency account within your existing finance tech-stack supports a more integrated alignment in finance workflows across domestic and global payments.

For example, if you invoice clients in USD, pay suppliers in EUR, and operate domestically in AUD, a multi-currency account lets you manage all three without constantly converting funds back and forth.

For finance leaders, this means greater control over FX exposure, improved cash visibility, and streamlined reconciliation among other operational efficiencies

Key benefits of a multi-currency account.

| Lower FX costs | Faster international payments | Improved cash flow visibility | Easier reconciliation | Smarter expense management |

| Competitive, transparent exchange rates | Access to local payment rails | One dashboard for all currencies alongside domestic payments | Accounting integrations | Corporate cards |

| Fewer repeated currency conversions | Reduced correspondent banking delays | Clear exposure tracking | Automated transaction matching | Built-in approval workflows |

Why multi-currency accounts matter more than ever.

Cross-border payments are growing rapidly as businesses expand globally, work with international contractors, and sell to customers worldwide. That growth can cause additional complexity, such as:

- FX markups hidden in exchange rates.

- Transfer delays through legacy banking networks.

- Manual reconciliation across multiple accounts.

- High administrative burden on finance teams.

A well-designed multi-currency account can reduce friction, improve visibility, and provide businesses more control over global cash flow.

So how does it work? A multi-currency account functions as a central financial hub.

For example, you can open a USD account with local US account details. You then share those details with customers to receive payments in USD and use the same funds to pay expenses in USD. Because the money stays in the same currency, you avoid unnecessary conversions and the fees that come with them.

1. Receive funds in foreign currencies

Many providers offer local account details (such as local routing numbers or IBANs) in major currencies, so your customers can pay you as if you had a domestic account in their country.

2. Hold balances without forced conversion

You don’t need to convert funds immediately. You can hold funds and wait for beneficial exchange rate movements.

3. Convert currencies strategically

Modern platforms offer real-time FX tools, allowing you to convert funds when it suits your cash flow and margin goals.

4. Send international payments

Pay suppliers, contractors, or employees directly in their local currency.

5. Integrate with accounting software

Leading providers sync transactions with platforms like Xero or QuickBooks Online, reducing manual entry and reconciliation time.

Bank based vs digital-first multi-currency accounts.

Not all multi-currency accounts are created equal. While both traditional banks and digital-first providers offer ways to manage foreign currencies, the structure, cost, and functionality can differ significantly.

For businesses operating across borders, understanding these differences is key to choosing a solution that supports efficiency, visibility, and growth.

The table comparison below highlights how bank-based multi-currency accounts stack up against modern digital-first alternatives.

| Feature | Traditional banks | Digital-first multi-currency providers |

| Account structure | Often require separate accounts for each currency | Multiple currencies managed under one login |

| Fees | Monthly maintenance fees may apply | Typically lower and more transparent fee structures |

| FX pricing | Usually wider FX margins, less transparency depending on the frequency and size of FX transfers | Competitive, transparent FX pricing |

| Automation and tools | Limited automation tools | Real-time currency tools and automation features |

| Cards | May not include integrated card solutions | Corporate virtual and physical debit cards available |

| Onboarding | Often requires in-branch or manual setup | Fully online onboarding |

| Expense and AP integration | Usually less integration with expense systems | Integrated expense management and accounts payable automation |

| Best suited for | Occasional foreign transactions | Growing, cross-border operations |

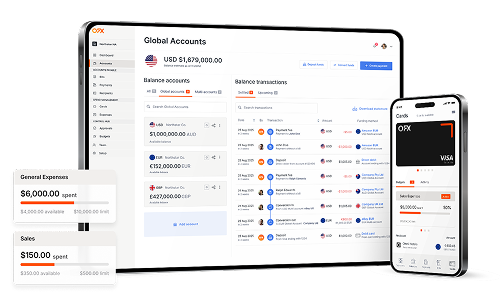

How OFX brings global and domestic payments together.

The OFX Global Business Account is designed to help simplify international financial management by uniting key cross-border and domestic payment capabilities on a single platform. Rather than juggling separate systems for banking, FX, cards, expense management, and accounting, OFX lets businesses handle everything in one place. This reduces complexity, risk, and admin overhead.

With a global business account you can:

- Hold, pay and receive funds in 30+ currencies with local account details for major markets like AUD, USD, GBP, EUR and CAD, making it easier to get paid and pay suppliers like a local.

- Send international transfers in 30+ currencies to 170+ countries at competitive foreign exchange rates.

- Issue corporate virtual Visa cards tied directly to your multi-currency balances, often with low or no FX fees when spending in held currencies.

- Use built-in approval workflows and spend controls before money leaves the business.

- Automate accounts payable and digital invoice processing via integrated tools that reduce manual entry.

- Sync with major accounting platforms for smooth reconciliation and real-time financial visibility.

- Access 24/7 human support and specialist guidance whenever you need it.

From this unified dashboard you can:

- Receive domestic and international payments with local details in key markets.

- Pay vendors locally or globally directly from the currency you hold.

- Manage team spending with cards and approval controls.

- Automate approvals and workflows before funds are released.

- Sync transactions with your accounting software for easier reconciliation.

- Monitor FX exposure and balances across all currencies.

For growing businesses, this consolidation reduces fragmentation, reduces errors, and streamlines how global and domestic payments are managed.

Too many tools, too many headaches? Finally, all your expenses and payments can be managed in one platform.

Managing currency risk: tools that matter.

Exchange rate fluctuations can directly impact profit margins. Advanced providers offer tools such as:

- Forward Contracts* – Lock in an exchange rate for a future transfer (up to 12 months), providing predictability for budgeting.

- Limit Orders** – Set a target rate and automatically convert when the market hits it.

These tools help transform FX from a reactive cost into a strategic advantage.

These FX solutions are included within the OFX Global Business Account, giving businesses more control over currency exposure.

*If you book a Forward Contract, it may mean losing out if the market rate improves because you’re contracted to settle at the agreed rate. This means you benefit if the market rate worsens, but you lose out if the market rate improves.

**If you book a Limit Order, it may mean losing out if the Market Rate continues to move above your Target Rate. There is no guarantee that your desired rate will be reached. Once the order is triggered, the transfer is binding and cannot be voided.

How to choose the right multi-currency account.

When comparing providers, focus on these six areas:

1. Supported currencies.

Does the account support the currencies you use today—and those you’ll need tomorrow?

2.FX transparency.

Are exchange rates competitive? Are margins clearly disclosed?

3. Transfer speed.

How quickly do international payments arrive?

4. Integrations.

Does the platform sync with your accounting or ERP system? Does the platform sync with your domestic payments?

5. Security and regulation.

Is the provider regulated? Do they offer multi-factor authentication and fraud monitoring?

6. Human support.

When something urgent happens, can you speak to a real person?

OFX combines digital efficiency with 24/7 phone support from real specialists.

How to get the most out of your multi-currency account.

A multi-currency account should be more than a place to hold foreign funds. It should actively streamline and strengthen your financial operations.

Start by using automation to your advantage. Set preferred FX rates or automated conversions to reduce the impact of market fluctuations and remove manual decision-making. This helps manage currency risk more strategically.

Introduce approval workflows to maintain control over team spending without slowing operations. Clear approval processes reduce errors and provide better oversight across currencies.

Virtual cards can further enhance control and visibility. They make it easier to track expenses by employee, team, or project, while simplifying reconciliation.

Scheduling recurring international payments helps you pay suppliers on time and reduces administrative workload. Integrating your account directly with accounting software also reduces manual data entry and speeds up month-end processes.

Finally, regularly reviewing your currency exposure allows you to make informed decisions about when to convert, hold, or deploy funds.

The real value of a multi-currency account isn’t just holding multiple currencies, it’s simplifying operations, improving visibility, and building a financial setup that supports global growth.

How to open a multi-currency account.

Most digital providers offer a streamlined onboarding process:

- Register online.

- Provide business and identity documentation.

- Complete compliance verification.

- Receive account details.

- Activate currencies as needed.

With OFX, most business accounts are approved within a few business days once documentation is complete, and you can begin managing global payments from one unified dashboard.

Turning global complexity into clarity.

A multi-currency account is more than a convenience, it’s a strategic tool for modern businesses operating in a global economy.

When implemented thoughtfully, it can:

- Reduce FX costs.

- Accelerate international payments.

- Improve cash flow visibility.

- Simplify reconciliation.

- Strengthen financial control.

The real advantage comes when your provider brings everything together: global transfers, domestic payments, FX tools, expense management, accounting integration, automation, and human support.

That’s where solutions like OFX make a meaningful difference: combining international and local financial management into one cohesive platform for growing businesses.

If managing cross-border payments feels more complicated than it should, it may be time to simplify.

Global growth should create opportunity, not administrative friction.

Manage currencies, payments and spend in one place