Will China’s economy get the expected reopening bump?

By the OFX team | 9 March 2023 | 5 minute read

After more than 2 years of severe lockdown, where its economy almost ground to a standstill, China is back to business and ready to trade.

But the most recent economic programme, delivered by outgoing Premier Li Keqiang, is conservative in its outlook – particularly when analysts expected China to announce a big stimulus package to make up for years of lost growth.

The government work report, delivered on the opening night of China’s National People’s Congress, opted for a conservative growth target of 5%, down from last year’s 5.5% — a figure that was missed by a wide margin due to lockdowns1.

“This year, it is essential to prioritize economic stability and pursue progress while ensuring stability,” Mr Li said, hosing down expectations that China would engage in a large-scale stimulus program to get the economy firing again.

For so-called commodity currencies (countries whose exports are dominated by commodities like coal, iron ore, or oil) it was negative news.

Without a pipeline of big infrastructure programs, and no announcement on stimulating real estate, iron ore (a key ingredient for steel) prices fell sharply2. That sent Australian mining companies down. The Aussie dollar then tracked downward by nearly 0.5% against the USD and euro. The New Zealand dollar, also considered a commodity currency, was down by a similar degree. Oil also fell on the less-than-anticipated growth figures.

Despite that fall, expectations are that China’s reopening should be positive for commodity currencies going forward with Goldman Sachs forecasting that iron ore prices should ramp up to $US150 a tonne over the next three months, up from the current $US120 a tonne3.

Chinese domestic growth returns but can it maintain momentum?

China watchers suggest the relatively conservative growth figures are a reflection that the economy has already bounced back somewhat since reopening. Factories have been ramping up, with the official index of manufacturing activity jumping month on month in February to its highest level in more than a decade. Service sector activity also rose4.

That’s good news for the economy and not a surprise, given restrictions have been lifted after years of stop-start lockdowns. But by not aiming for a higher growth rate, the interpretation is that China doesn’t want to push for growth at the expense of economic stability.

A separate report, issued by China’s National Development and Reform Commission called out high debt levels in the property sector. It also indicated the government would discourage housing speculation. Local governments also took on too much debt and need financial reform.

“There are still quite a few factors restraining the recovery and growth of consumption. Resuming growth in real estate investment is an uphill battle,” the report said.

“Some local governments are finding economic recovery difficult and are facing prominent fiscal imbalances. Debt risks from local governments’ financing platforms need to be addressed immediately5.”

In all, that paints a picture of a government that will not be splashing unsustainable amounts of cash at two of the growth areas — property construction and local infrastructure projects — that were so fundamental to commodity currencies.

Instead, China is hoping that it can attract back investment from foreign firms that were such a driving force for rising domestic wages and prosperity.

“We should ensure national treatment for foreign-funded companies … We should improve services for foreign-funded companies and facilitate the launch of landmark foreign-funded projects,” Li Keqiang said in the national work report. “With a vast and open market, China is sure to provide even greater business opportunities for foreign companies in China“.

We should ensure national treatment for foreign-funded companies … We should improve services for foreign-funded companies and facilitate the launch of landmark foreign-funded projects, said outgoing Premier, Li Keqiang, in the national work report.

China will have some convincing to do after debilitating lockdowns and political tensions with the US. According to the American Chamber of Commerce in China, for the first time in 25 years, China was no longer considered by most of its member companies to be a top-three investment destination6. The US has also been financing the reshoring of manufacturing of major industries, particularly in high-tech areas, that have been such a boon to the Chinese economy. For example, the US had an estimated $210 billion in announced domestic investment in electric vehicle and battery factories by January of this year, ahead of China, and the rest of the world in terms of battery production7.

How other foreign investors view returning to China will be a key area to watch going forward.

Which way will the trade winds blow?

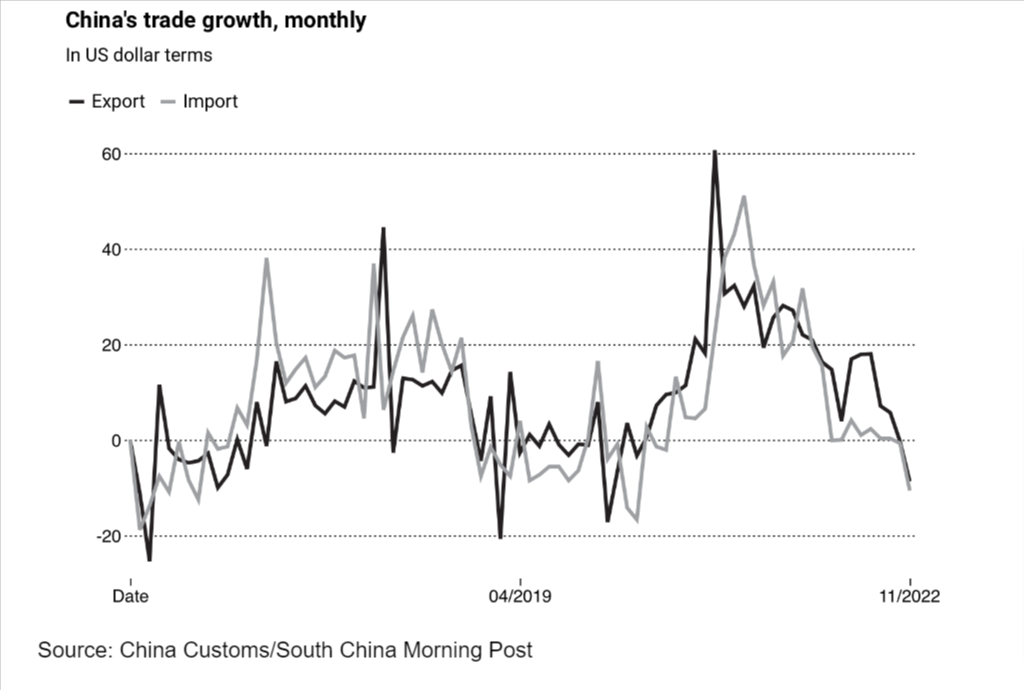

Data on trade between China and regional partners suggest that the reopening has not led to a significant bump in consumption.

China’s growth from exports has also shown weakness. Exports from China slumped 10% year on year in December, the steepest fall in exports in three years, amid cooling global demand as interest rates rise to control inflation8.

If China fails to find a rebound in exports just as it is ramping up production, it may place downward pressure on the RMB.

Not only that, but if China can’t leap out of the blocks in terms of growth, it may mean that the knock-on effect for the global economy will also fail to occur, meaning financial institutions will continue to prefer the safety of traditional safe haven economies with relatively high interest rates. That would be positive for currencies such as the euro, USD and Swiss Franc.

OFXpert, Jake Trask, shares his view now that China has reopened

Should the Chinese economy rebound significantly this year it will create a welcome tailwind for global stock markets which have been battered by the ongoing interest rate hikes from the US Federal Reserve. The Chinese government recently set its lowest annual growth target in 30 years of 5%. Should it exceed this, and manufacturing Purchasing Manager’s Index (PMI) numbers/data continue to show expansion, then this may create less demand for the safe haven US dollar and will benefit commodity currencies such as the Aussie and Kiwi. That said, recent comments from Federal Reserve Chairman, Jay Powell, indicate that they intend to continue to raise interest rates higher than previously forecast, to combat persistently above-target inflation. Should this come to fruition, the dollar bull will likely carry on for much of 2023.

References

- https://www.wsj.com/articles/china-sets-economic-growth-target-of-around-5-for-the-year-88eaff89

- https://www.theaustralian.com.au/business/mining-energy/iron-ore-tumbles-as-chinas-national-peoples-congress-sets-modest-growth-target-no-stimulus/news-story/52d0536233bc3e3c1f4fbfa61dc6bcaf

- https://www.afr.com/markets/equity-markets/goldman-a-buy-on-rio-as-iron-ore-bull-case-strengthens-20230306-p5cpnz

- https://www.nytimes.com/2023/03/01/business/china-factories-economy.html

- https://www.scmp.com/economy/china-economy/article/3212438/chinas-two-sessions-2023-outgoing-premier-vows-even-greater-business-opportunities-foreign

- https://www.scmp.com/economy/china-economy/article/3212438/chinas-two-sessions-2023-outgoing-premier-vows-even-greater-business-opportunities-foreign

- https://www.forbes.com/sites/willyshih/2023/02/22/the-inflation-reduction-act-will-bring-some-manufacturing-back-to-the-us/?sh=1e3c8dfdb544

- https://tradingeconomics.com/china/exports-yoy#:~:text=Exports%20YoY%20in%20China%20averaged,data%20for%20China%20Exports%20YoY