The flight to safety

How investor behaviour impacts currency in times of volatility

July 2020

Crises that affect world markets tend to hit with little warning and major impacts, leaving everyone from traders and investors rushing to find ways to limit their losses while the catastrophe unfolds.

The various crises we have seen in the last 50 years have happened for many different reasons, but the reaction to them has been much the same. Investors look to limit exposure to equities – which are shares in companies, so called because you get ‘equity’ in a company when you buy shares1– and move towards bonds and cash while the crisis plays out.

Sheltering money in ‘safe haven’ currencies is a next step, with the US dollar, Swiss franc and the Japanese yen typically appreciating during difficult times for global markets. These currencies are considered safe havens because they are highly liquid, and tend to appreciate in times of crisis. The US dollar particularly is the currency that many business deals worldwide are conducted in, which also makes it appealing in a crisis2.

Why move away from equities?

When volatility hits, you might need to take strong, far-reaching, decisive action to have the best chance of limiting the damage to your investment portfolio, and/or your business. Equities tend to be hit first when there is a crisis – during the COVID-19 pandemic for example, travel companies were particularly badly hit. EasyJet and Carnival both fell out of the FTSE 100 as they lost 45% and 67% respectively of their value, which meant they no longer qualified to be one of the UK’s top 100 companies3.

When a crisis hits, investors want to mitigate their losses, so look for better short-term investments. During the COVID-19 crisis, a number of companies decided to cut or completely stop their dividends to shareholders. This matters – it is a main way investors make money from shares. Even stalwart payers have acted, such as Royal Dutch Shell which is cutting its dividend for the first time since WWII4. In total, around a third of companies in Britain’s FTSE 100 scrapped their dividend altogether5.

Investors move to bonds – but not as we know it

Traditionally, the move away from riskier stocks and shares would be towards safer government bonds which are backed by the country’s taxpayer – that is still happening. Yet in the current crisis, yields are considerably lower than ‘normal’. However, one area that is seeing considerable growth is social bonds6 as investors are able to get higher returns while also helping communities during the crisis.

What does this mean for businesses trading overseas?

The flight to safety – which includes putting money into cash, safe haven currencies and bonds – is the result of investors looking to move out of assets that will fluctuate violently or currencies that will be negatively impacted by a crisis.

As safe haven currencies are known to appreciate during difficult economic times, businesses trading in one of the safe haven currencies will need to bear this in mind. A transfer to one of these currencies could cost them more during a crisis. This is where planning ahead and building a currency strategy can help to minimise costs and increase profits

Ask an OFXpert

Our OFXpert Hamish Muress answers questions on the issues impacting currency markets right now.

Q. How do countries respond when faced with a major economic problem?

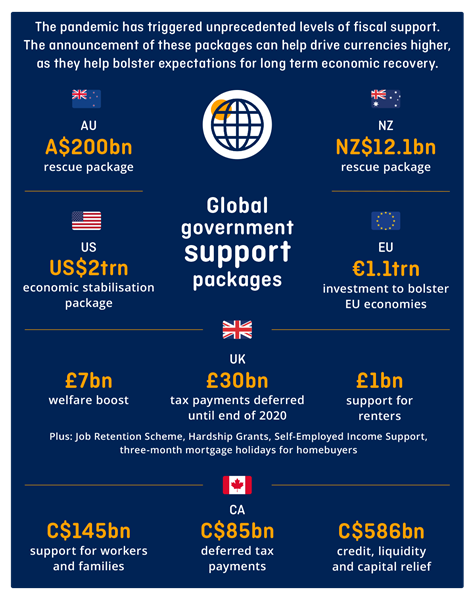

A. When it comes to stabilising economies, the most important thing is to ensure there is sufficient money in the economy to keep businesses and people buying goods and services. Cutting interest rates – which was one of the first things central banks around the world did as it became obvious that COVID-19 was going to be a global pandemic – reduces the amount everyone needs to pay on debt. This leaves more money available to buy items, which helps to keep GDP elevated.

The other thing central banks do is implement ‘quantitative easing’ (QE) where they put more money into the economy by effectively printing money.

During February and March 2020, the US Federal Reserve also set up unprecedented ‘swap lines’ with other central banks to support liquidity in global markets. These are used at times of financial stress to help foreign central banks provide US dollar funding to institutions outside the US during times of economic difficulty. One thing that has been a relief for markets is confirmation from the US Federal Reserve that the US won’t move to negative interest rates.

Q. So when the recovery comes, would we expect to see these measures reversed?

A. Yes, but they are unlikely to all be unwound at the same time or the same rate. For example, QE is usually reduced before interest rates start to rise. But as there is set to be what the UK Chancellor described as “a severe recession, the likes of which we have not seen”8, we could be waiting some time for this to begin.

In fact, the likelihood is we will see a ‘new normal’ for interest rates. Long gone are the days when G10 rates could reach double figures and the fact that they didn’t emerge from the ultra-low rates imposed after the financial crisis of 2008 before the COVID-19 pandemic hit 12 years later will reinforce this thinking.

Download the OFX Currency Outlook

Learn more in the latest edition of the OFX Currency Outlook. It’s been produced to help you navigate market movements today, and to understand what to watch out for in the coming months.