Euro falls to parity against US dollar, what’s next?

August 2022

A

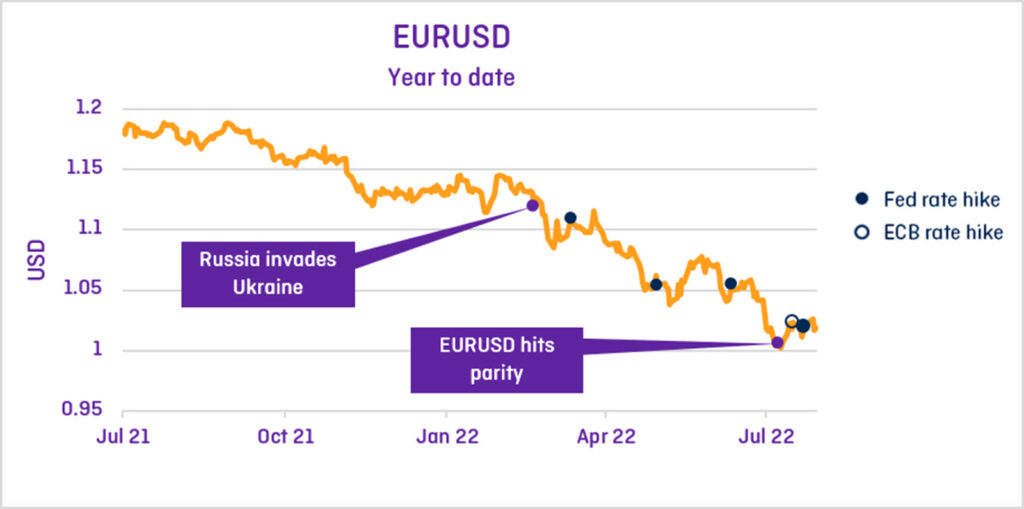

In mid-July one of the currency world’s rarest events happened. The euro dropped to parity against the US dollar.

€1 < $1 has only happened once before, and that was in the early days of the euro’s existence. Back then, between 1999 and 2002, the dot com crash sent investors in search of safe havens1 — namely the US dollar — and back then the euro, as a new currency was still an experiment with some proving to do.

But since December 2002 the euro has been higher, and often significantly so than the USD. At its peak, during the global financial crisis in 2008, the euro hit a high of $1.60 relative to the dollar, demonstrating the European currency’s own position as a safe haven when the credit crisis almost brought down the US banking system and forced the US Federal Reserve to drastically shore up the country’s financial footing on top of slashing interest rates.

Back then the crisis originated in the US. This time the crisis is on Europe’s doorstep.

Dollar up, euro down: How did we get here?

The synchronised global response to COVID-19 is well and truly over. In the US, low rates and huge government stimulus have pushed the economy into overdrive, whereas Europe continues to limp slowly back to pre-pandemic growth levels. Adding more complexity to an already tricky scenario, the Eurozone economy has also been impacted by the invasion of Ukraine, particularly with regard to energy prices.

Main reasons for USD strength

- After keeping interest rates low for longer than, in hindsight, they should have, the US Federal Reserve is now on an inflation-busting crusade. In mid-July inflation figures for June showed the highest gain in prices in 40 years at 9.1% year-on-year.2 The Fed is already working hard to bring inflation down, raising rates from almost zero to 2.5% in just five months. A Fed board member said in early August that the bank was “nowhere near done” in getting inflation down,3 effectively priming the market for more rate rises. That sent bond yields up in anticipation. As interest rates go up, US dollar-denominated assets become a preferred investment, driving up the dollar.

- Rising interest rates around the world, and stubborn inflation, are contributing to fears of recession in a number of countries. As flagged in our last article, the US may already technically be in a recession,4 the UK is likely in one, and Europe is heading that way by year’s end. Facing the prospect of slowing growth and its impact on asset prices, investors tend to prefer safe-haven assets in large, liquid, stable jurisdictions. Usually that would be both the US and Europe, but with Europe’s more precarious economic environment due to the war in Ukraine, investors are opting to put their money in the US over Europe and buying the dollar instead of the euro.

Main reasons for EUR weakness

- While the US Federal Reserve has been aggressively raising interest rates, the European Central bank has been far more dovish (or accommodative). Interest rates had already gone up by 1.5% in the US before the ECB eventually determined it had to do something about inflation, raising rates by 0.5% in late July.5 While the US Fed is signalling it will raise rates even further, the ECB is in a more challenging position. With 19 member states, the blunt instrument of interest rate rises may have a far harsher impact, particularly on those member countries burdened with high government debt. Raising interest rates will make that debt both harder to pay back, as well as reduce the ability of those countries to borrow further, which would put downward pressure on parts of the Eurozone economy.

- Rising inflation is the key concern of most central banks that are currently in a tightening cycle, and one of the biggest drivers of inflation has been energy prices. The war in Ukraine has been particularly inflationary for Europe which is reliant on Russian gas for its energy supply. Inflation hit a record high of 8.9% in July on the back of higher energy costs.6 Whereas above-target inflation in other regions is a supply and demand issue (higher demand raises prices, higher interest rates dampen demand), in Europe, it is the cutting off of gas from Russia that is doing significant damage. The knock-on effect of reduced energy supply may naturally slow Europe’s economy down, meaning interest rates may not rise as far or as fast as the US to get the economy under control. If investors believe the energy issue may not be resolved, they may opt to move their money to the safer-haven of the US dollar.

What to watch

Currency markets will be looking to further guidance from the Fed about how long it will continue its inflation-busting ways. Federal Reserve board members have already signalled that rates may need to go as high as 4% from the current 2.5% over the next year7 which would continue to put upward pressure on the US dollar, certainly relative to the Euro.

However, inflation remains stubbornly high and the US economy is slowing, so investors will be highly attuned to any indication that higher interest rates are starting to bite. This might cause the Fed to change course, which would lessen the yield appeal of the US dollar.

We should expect to hear more in late August, at the Federal Reserve’s Jackson Hole symposium — basically a strategy “away day” for central banks. Markets will be anticipating a scene-setting speech from Fed Chairman Jerome Powell where he will hopefully shed some light on the outlook for Fed monetary policy setting.

In Europe, the war in Ukraine, now approaching its sixth month, continues to act as a destabilizing force for the Eurozone economy. Gas supply is clearly being used by Vladimir Putin in a game of brinkmanship. At the start of August, Russia cut off supply to Latvia,8 while gas supplies to Germany via the Nord Stream 1 pipeline have been restricted to just 20% of capacity.9 Europe is now attempting to lower gas consumption by 15% from August to March to prepare for winter.10 Finding a solution will be critical for the Eurozone. As France’s minister for energy transition, Agnès Pannier-Runacher cautioned, the whole European economy is vulnerable: “Our industrial chains are completely interdependent: if the chemical industry in Germany coughs, the whole of European industry could come to a halt.”11

References

- https://qz.com/2187678/the-euro-hit-parity-with-the-dollar-for-the-first-time-in-20-years/

- https://www.nbcnews.com/business/economy/us-inflation-june-2022-consumer-price-index-rcna37897

- https://www.afr.com/markets/debt-markets/inflation-hawks-dampen-hopes-of-fed-easing-to-push-shares-lower-20220803-p5b6wi

- #region-link-doesnt-exist

- https://www.theguardian.com/business/2022/jul/21/european-central-bank-raises-interest-rates-for-first-time-in-11-years

- https://www.theguardian.com/business/2022/jul/29/eurozone-inflation-record-energy-prices-growth

- https://www.afr.com/markets/debt-markets/inflation-hawks-dampen-hopes-of-fed-easing-to-push-shares-lower-20220803-p5b6wi

- https://impakter.com/russia-energy-war-europe-cuts-gas-latvia/

- https://www.reuters.com/business/energy/kremlin-nord-stream-1-turbine-be-installed-volumes-will-adjust-2022-07-25/

- https://www.theguardian.com/business/2022/jul/26/eu-agrees-plan-to-reduce-gas-use-over-russia-supply-fears

- https://www.theguardian.com/business/2022/jul/26/eu-agrees-plan-to-reduce-gas-use-over-russia-supply-fears

Download the OFX Currency Outlook

Learn more in the latest edition of the OFX Currency Outlook. It’s been produced to help you navigate market movements today, and to understand what to watch out for in the coming months.