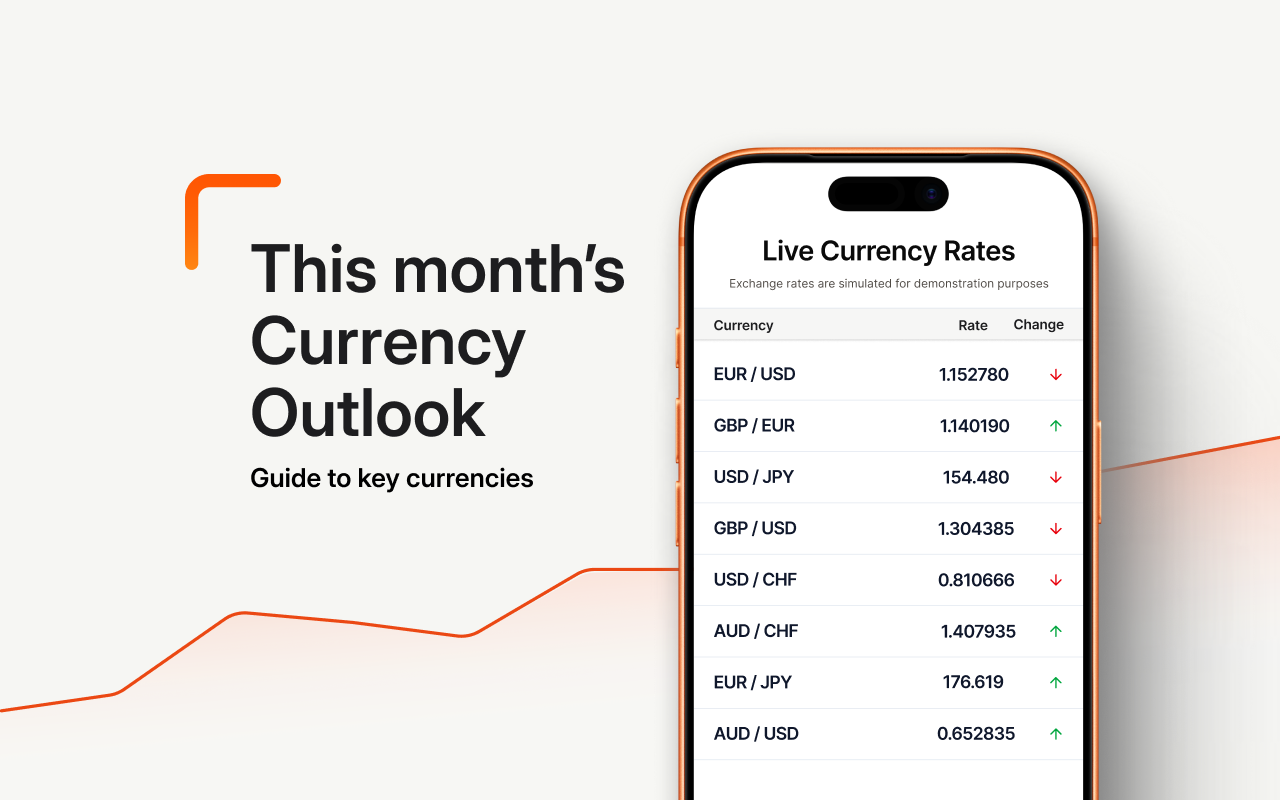

Read this month’s Currency Outlook

Find out what could impact exchange rates for key currencies in the month ahead in our cheat sheet.

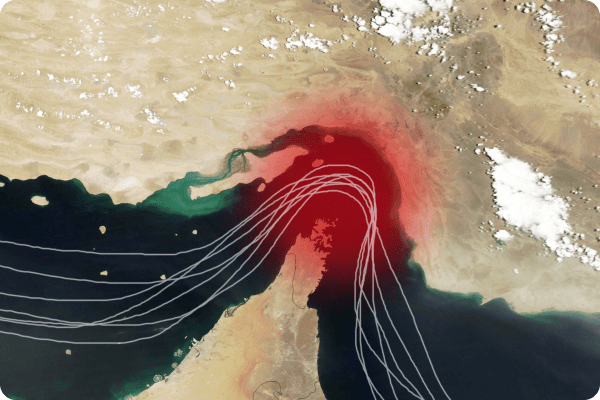

Impact of the Strait of Hormuz on central bank decisions.

Read our latest currency news and keep informed on the global factors that can impact future currency movements in the coming month.

Currency chart

From

To

CAD/USDcurrency chart: 1.00 CAD = 0.7122 USD