Impact of the Strait of Hormuz on central bank decisions.

By the OFX team | 12 May 2026 | 6 minute read

In the world of foreign exchange, there are four central banks that really matter; and all of them faced challenging decisions on interest rates in late April.

The Federal Reserve (Fed), the Bank of England (BoE), the European Central Bank (ECB) and the Bank of Japan (BoJ) all find themselves dealing with an exogenous problem they can’t control: increased energy prices flowing through as a result of the Middle East conflict.

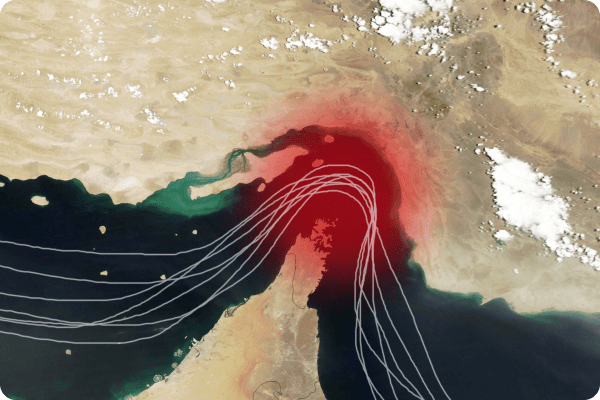

Not only do central banks not control the price of the energy inputs into their economies, they do not control when the Strait of Hormuz fully re-opens, nor when constrained energy flows get turned back on.

The surge in input costs threatens to undo the progress made in tailoring rate settings to long-term inflation expectations.

This uncertainty was high on the agenda at their respective April meetings.

Before the big four central banks met, Laura Cooper, Head of Macro Credit and Global Investment Strategist at global investment firm Nuveen, put it aptly: they were “four central banks pausing at the same crossroads.” Cooper expected them all to hold, but for different reasons: “The Fed is expected to hold with conviction, the ECB with caution, the BoE with uncertainty and the BoJ with hesitation,” she said.

Cooper was right on the group’s stasis.

On 29 April, the Bank of Japan – considered to have the most committed tightening bias in global markets, coming off the lowest base of its major peers – opted to hold at 0.75%, the highest level since September 1995. Illustrating the tightening pressure, three board members (of nine) dissented, urging a hike to 1.0% amid mounting price pressures.

Coming out of its April 28–29, 2026, meeting, the Federal Reserve kept interest rates steady at 3.5%–3.75%, marking the third consecutive meeting without a change. The Fed had even more arguments than the BoJ, with four out of the twelve members of the Open Market Committee voting against the decision, the highest level of dissent since 1992.1 In his press conference, Fed Chairman, Jerome Powell signalled a cautious “wait-and-see” approach.

The Fed statement included reference to an “easing bias” (that is, an inclination to lower rates). Three of the “no” votes came from regional presidents Beth Hammack of Cleveland, Neel Kashkari of Minneapolis and Lorie Logan of Dallas, who said they agreed with the hold but “did not support the inclusion of an easing bias in the statement at this time.”2 Chair Powell argued that the uncertainty surrounding the oil price shock made this an inopportune moment to adjust the Fed’s wording.

On April 30, the European Central Bank and the Bank of England also announced they would hold rates steady.

The Bank of England Monetary Policy Committee (MPC) voted 8-1 to hold interest rates at 3.75%, citing inflationary pressures from the Iran war; chief economist Huw Pill voted for a 0.25 percentage point increase to 4%, while the majority kept rates steady for a third consecutive meeting.3 As for the ECB, it kept its three key interest rates at their lowest level for more than two years, also for the third straight meeting4 (the ECB does not typically publish exact tallies of Governing Council votes.)

None of these outcomes would have been predicted before the Middle East conflict broke out, but the content of the central banks’ deliberations has been taken over by the surging energy prices and their potential to dampen growth and push inflation higher, and the question of how long the conflict will last.

What may have been hawkish outlooks on the part of the central banks have had to adapt to what geopolitics is giving them.

In all four cases, to varying extents, data suggests their economies need help, but first they have to deal with the renewed inflationary pressures before supporting growth.

It is a difficult time for them. Policymakers may not be behind the curve this time, but they are “unsure where the curve is,” said Cooper.

Similar to its peers’ situations, the economic backdrop that the Federal Reserve faces in the US is highly uncertain. Inflation has risen to 3.3% – well above the Fed’s 2% target rate – driven partly by higher energy prices, while hiring has slowed sharply.5 There is no clarity on how the supply-chain impacts of the Middle East conflict may affect US GDP, but the imperative is to support growth: according to the Federal Reserve’s Summary of Economic Projections (SEP) released in March 2026, officials projected a 2.4% real GDP growth rate for 2026. First-quarter (March 2026) GDP grew at an annualised rate of 2.0%; commercial banks’ full-year (that is, annualised growth by the fourth quarter) GDP expectations range from 2% (J. P. Morgan) to 2.5% (Goldman Sachs.)6 The Fed also faces a leadership transition from current Chair Jerome Powell to Kevin Warsh ahead of the June meeting, but that is a sideshow to the “higher for longer” feeling that markets are pricing-in for US rates.

For the ECB, energy-price vulnerability is the big problem, with a far less-resilient economy than that of the US. April purchasing managers index (PMI) figures surprised to the downside, as activity in the Eurozone’s dominant services sector contracted for the first time in almost a year, hit by weakening demand and deteriorating export business, as the Middle East conflict weighed on consumer-facing sectors.7

Where Eurozone GDP grew by 1.5% in 2025, 2026 forecasts have been cut to virtually half that, with a recovery pushed to next year.8 The ECB’s hold decision may have seemed dovish, but President Christine Lagarde emphasised that a rate hike was discussed and could come as soon as June, depending on the data.

The Bank of England faces a cocktail of energy-cost rises, deteriorating labour market, government spending rather than private-sector strength generating what robust data there is, and political uncertainty to top it off. Since mid-2024, rates have been cut six times, and markets had anticipated further easing in 2025 before the conflict in the Middle East disrupted the outlook. Higher energy costs are already feeding through to households and businesses, and the BoE is negotiating a tricky balancing act that “leans towards cuts, not hikes,” according to Cooper. After ‘spooking markets’ with its unanimous and hawkish ‘ready to act’ stance last month, the Bank of England does not have a credible case for near-term rate hikes,” she says.

Wealth advice firm Hoxton Wealth says this trio of central banks are in a similar bind. “All three would prefer to begin easing policy; the reason they cannot is oil,” the firm says.

The Bank of Japan typically deals with a different set of challenges to its Atlantic peers, and the present is no different. It faces significant pressure to lift interest rates, driven by a stubbornly weak yen and rising import costs from geopolitical uncertainty. The soft yen has increased the cost of importing raw materials and energy, hurting corporate profits and household incomes.

As it decided to hold, the BoJ sharply raised its 2026 inflation forecast from 1.9% to 2.8%, simultaneously slashing its GDP growth forecasts for the year from 1% to 0.5% – starkly highlighting the risks from increased energy and raw material costs.9 Arguably more than any major economy, Japan is staring at stagflation risk, and markets increasingly lean to a potential rate hike in June.

The “big four” central banks’ future rate decisions will likely continue to be influenced by the Strait of Hormuz, and more generally, how quickly energy flows can return to what the world had come to view as normal.