Fed’s go-slow approach likely to keep USD weaker, for now

September 2021

A sleepy mountain resort amid the ski fields of Wyoming becomes the focus of the currency world’s attention for a few days every year. It’s host to an economic symposium sponsored by the Federal Reserve Bank of Kansas City that attracts central bankers and finance ministers from around the world to prognosticate on the big issues of the day. This year’s event was held virtually due to Covid-19 but it was scrutinised just as closely by market participants.

Jackson Hole is known for wild variations in temperature, but in his keynote, US Federal Reserve Chairman Jay Powell served up a “not too hot, not too cold” speech that markets lapped up.

Powell had been trying to find the middle ground amid a Federal Reserve Board that is becoming increasingly split between hawks – those who believe interest rates should rise – and doves who believe they shouldn’t.

The hawks are particularly concerned that the continued use of quantitative easing (QE), a method of purchasing bonds to stimulate the economy – must end soon. Otherwise, the central bank could “really get into trouble” if it followed a “go-slow” approach to fighting inflation.1

But the doves feel that moving too fast, too soon could derail the US’s economic recovery, particularly as the virulent Delta strain sweeps through the country.

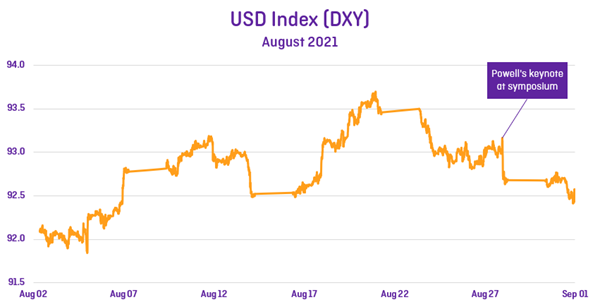

The market had expected Powell to side more with hawks and give a clearer view of when the Fed would start ‘tapering’ QE and putting upward pressure on interest rates. Indeed, so sure were hedge funds that Powell’s statement would cause the US dollar to rise that they invested heavily in the outcome, pouring $US8.4 billion into the US dollar in the lead to the symposium, compared to just $800 million the previous week.2

It was the culmination of a 3% rise in the greenback against a basket of currencies over the last three months, and an indicator of the strengthening of the US economy relative to peers.

Instead, Powell split the middle between the doves and the hawks by flagging the need for tapering but without setting a timetable for when.

As OFX Treasurer Sebastian Schinkel notes, “Powell somehow managed to acknowledge both sides of the equation and although he conceded on tapering, he made it clear that it will not translate into interest rate hikes ‘for which we have articulated a different and more stringent test’”.

That sent the US stock market to new highs and caused bond yields to fall as investors cheered the prospect of continued stimulus. (A higher stock market and lower bond yields are typically both correlated to a lower US dollar.)

The US dollar index fell 0.5% following the speech as investors sold off the dollar in search of better returns elsewhere.

Two factors appear to have swayed the Fed’s thinking.

First, the Delta variant continues to impact the US economy, with the Southeast particularly badly affected. Many workers still haven’t returned to offices, meaning central business districts still haven’t fully recovered. Consumer sentiment recorded its biggest fall in a decade3 in August as the high infection rate quashed hopes of a full reopening.

A record number of job openings is also crimping the economy, as workers continue to stay home out of fear for their health, or because unemployment benefits continue to be generous relative to pre-Covid.4 The Federal Reserve has stated that it will keep rates accommodative until it sees the economy return to “maximum employment”5, a subjective term which is more based on art than science. Disappointing August employment figures indicated the Fed is still yet to reach that target. That hiring gap along with supply chain issues due to Delta is filtering through to higher inflation. Fuel, food and many services are seeing price spikes,6 another factor behind tumbling consumer sentiment.

So, the Federal Reserve needs to determine whether rising inflation is an issue that will need to be controlled with interest rates or if it is just a transitory phase as the economy returns to normal.

Growth rates remain high at 6.6% annualised, according to the latest quarterly data and in a normal world the Fed would be putting on the brakes by raising interest rates. That would likely push the US dollar higher relative to peers but, for now, it appears the Fed is less worried about the economy getting too hot than the prospect of it going cold.

The next Federal Reserve meeting on September 22, may be the trigger for more currency volatility depending on whether the hawks or the doves gain ascendancy.

1https://www.reuters.com/world/us/fed-minutes-likely-detail-bond-buying-taper-talks-inflation-worries-2021-08-18/

2https://www.reuters.com/article/markets-funds-fed/column-feds-powell-wrongfoots-hedge-funds-on-dollar-bonds-jamie-mcgeever-idUSL8N2PY48K

3http://www.sca.isr.umich.edu/

4https://www.nytimes.com/2021/08/31/business/economy/biden-economy.html

5https://www.wsj.com/articles/fed-faces-new-challenge-spelling-out-employment-goals-11630229402

6https://www.nytimes.com/2021/07/28/business/economy/inflation-republicans-biden-spending.html

Download the OFX Currency Outlook

Learn more in the latest edition of the OFX Currency Outlook. It’s been produced to help you navigate market movements today, and to understand what to watch out for in the coming months.